Management Accounting

| ✓ Paper Type: Free Assignment | ✓ Study Level: University / Undergraduate |

| ✓ Wordcount: 1526 words | ✓ Published: 12 Aug 2019 |

PART 1:

Management accounting techniques

| Budget | Actual | Variances | |||||||||||

| Units | £ per unit | £ Total | Units | £ per unit | £ Total | Standard | Units | £ per unit | £ Total | Against standard | |||

| Sales | 4,000.00 | 273.00 | 1,092,000 | 3,200 | 300.00 | 960,000 | 873,600 | -800 | 27.00 | -132,000 | 864,000 | ||

| Based on ‘normal’ level of production | |||||||||||||

| Direct Materials (kg) | 7 | 70.00 | 280,000 | 10 | 90.00 | 288,000 | 224,000 | -3 | (30.00) | -8,000 | 64,000 | ||

| Direct Labour (hrs) | 10 | 90.00 | 360,000 | 9.25 | 83.25 | 266,400 | 288,000 | 0.75 | 6.75 | 93,600 | -21,600 | ||

| Direct Expenses | 30.00 | 120,000 | 32.50 | 104,000 | 96,000 | (2.50) | 10,000 | 8,000 | |||||

| Prime Cost | 190.00 | 760,000 | 205.75 | 658,400 | 608,000 | (15.75) | 101,600 | 50,000 | |||||

| Fixed Admin Costs | 5.00 | 20,000 | 6.25 | 20,000 | 20,000 | (1.25) | 0 | 0 | |||||

| Other Overheads | 15.00 | 60,000 | 9.25 | 29,600 | 60,000 | 5.75 | 30,400 | -30,400 | |||||

| Total Fixed Costs | 20.00 | 80,000 | 15.50 | 49,600 | 80,000 | 4.50 | 30,400 | -30,400 | |||||

| Total Cost | 210.00 | 840,000 | 221.25 | 708,000 | 688,000 | (11.25) | 132,000 | 19,600 | |||||

| Profit | 63.00 | 252,000 | 78.75 | 252,000 | 185,600 | 15.75 | 0 | 66,400 | |||||

| Contribution | 83.00 | 94.25 | |||||||||||

| Break -even point | 964 | 562.26 | |||||||||||

| Margin of safety | 3,036 | 2,638 |

The profit between the budgeted cost 252,000£ and the actual cost 252,000£ is by accident the same amount. Cost card above explains all the situation within organisation LSEC Ltd. Company achieved the same profit 252,000£, even though was expecting less, because of the smaller amount in the sales 3,200 units. LSEC Ltd. budgeted forecast at 4,000 circuit board level production per month, with the price 273£ per unit and revenue of 1,092,000£. Primarily it was budgeted that total cost per month will be 840,000£, with the profit of 252,000£ per month. However, after one month of sales LESC Ltd. was informed that 3,200 circuit boards with revenue of 960,000£. Budgeted calculations were predicted for 4000 units actually was sold 3,200units. Budgeted plan next to actual sales can specify more some of the costs. Budgeted cost for direct materials was lower than actual, because actually it costed company 8,000£ more, however direct labour and direct expenses were budgeted too high. Variances of total cost 132,000£. Even though direct material from actual cost was higher LSEC Ltd. producing 3,200 of circuit boards, gains 132,000£ from budgeted total cost, because overall total cost was 132,000£ less then budgeted. With production of 3,200 units LSEC Ltd. spend less money for total cost, thanks to the variances in the direct labour and direct expenses. Provided cost card must help in decision-making, because is complex from relevant information’s. Job costing system can allow to get detailed information as well as calculate profit earned on jobs.

PART 2:

Understanding of management accounting systems

This report aims to promote understanding management accounting in LSEC Ltd.

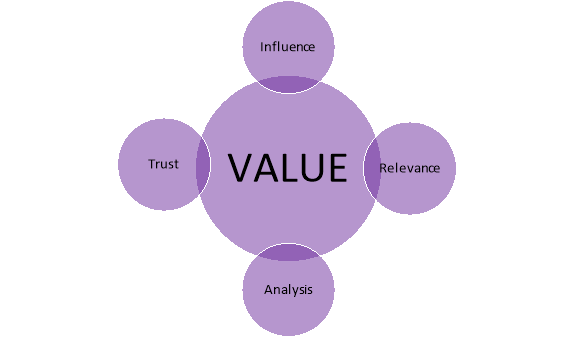

Management accounting forces to look into the future. It presents information of internal management and aims to provide data which is relevant to making business decision and fulfil organisational objectives for now and in the future. Starting point of this information it’s a detailed analysis of individual cost components of product and services. This detailed information can be used to plan what the business will do and what decision it will make to allow to operate profitable in the future. There are four principles focused on four outcomes. Influence, Relevance, Analysis and Trust.

Management accounting starts and ends with conversation. Communication delivers observation that is influential. Collection and classification of data is main function of accounting department. Information collected has to be relevant. Relevance principle includes identification, collection, validation, and store of that information. Not every information is relevant. The information collected is used by the management for making decisions. The third principle is to analyse the impact on value. Management accounting takes into account the analysed information together with the way to produce values. It focus on any risk, cost or chances. Last one, trust is build by stewardship. People who are working in management accounting must be integral, ethical and sustainable. This makes the decision making process more objective.

Financial accounting it’s a process of preparing financial statements, balance sheets that organisations uses to show their financial performance from the past. Information that is showed to the people outside the company, including public, customers, investors, creditors, suppliers.

DIFFERENCES

| MANAGEMENT ACCOUNTING | FINANCIAL ACCOUNTING |

| current and future information (forecasting, budgeting) | past information (statements) |

| internal audience (company) | external audience (public) |

| financial and non-financial information | financial information |

| no standards or rules | set of standards and regulations |

Management accounting systems mainly focus on following the costs connected with production of services or products. Different types of systems helps the management to prepare reports which will help to make decision. Reports are provided with accurate, financial and reliable information. Each of the systems provide different method for following cost for a company to produce services and products at the lowest cost. There are different types of management accounting systems. Business exist to make profit. Without knowing costs will be not possible for the business to set the selling price higher then the cost incurred. Cost accounting systems help organisations to estimate the cost of their products for profit. When the selling price exceeds the costs a profit is made. There are two main cost accounting systems: the job order costing and the process costing. Job order costing needs to accumulate three types of information: cost of direct material that is used, cost of the direct labour what is used to do the job, and overhead, means system assigns overhead costs to cost pools. Job order costing helps to count manufacturing cost for each individual product. It’s good for the companies which are producing unique products and special orders. Process costing it’s a system which accumulate manufacturing cost for each process. Job costing it’s a system which helps to assign cost for each individual product cost. System that helps in the evaluation of the quality of work done. Inventory management system helps keep

tracking at the end of each accounting year, unsold items of production. It helps to owners of the business to know when is the time to buy more materials or restock products. Management accounting systems benefits an organisation.

Management accounting is a key role in finance, management accountant must achieve a series of task to ensure organisation’s financial safety. Analysing financial information is equally important in achieving organisational objectives. Financial information translated into report is helping into decision-making.

Forecasting it’s a development of goals. Planning process take place because it helps the company achieve its goals. Management accounting help create company budget thanks to which the organisation knows estimated cost, profit.. Planned future sales or allows the company to grow. Organising is a structuring the tasks. Shared responsibility allows much easier attain objectives of the company. Organising includes accuracy regarding the division of responsibility. Process of organising requires clear assignment of authority with division of resources covering all organisation to accomplish the same goals. However management accounting is also controlling department activities. Control it’s a process where continuous monitoring, correcting has a place in order to improve. Together with that process feedback is given, and that information lets company decide to stop some of the activities or continue with improvement. In the controlling function management accounting helps by preparing reports. Previously prepared reports regarding budgeted costs are compared with actual costs to calculate variances. Three management accounting functions described above are inseparable in making decisions. Process of making decision involves finding out the problem and deciding is it required any action to take. Before decision will be taken the objective must be defined, for example maximising profit of the company. In this process many other tasks is done like shortlisting possible alternative actions.

Management accounting plays very important role within an organisation. It helps in supporting, planning, controlling or decision making. Management accounting systems benefit organisation with advanced information to plan the costs. LSEC Ltd. can be certain that operations performed in the company are effective and efficient. Reports with variances clarifying much faster. Management accounting makes some of the objectives much easier to achieve. Department that by preparing budgeting reports, and controlling budget increase level of profitability for the company. The use of that system make it much uncomplicated for the organisation to remove high or extra expenses for performing dynamic operations. One of the most important benefits to the organisation though management accounting is simplified decision-making. Caused by detailed reports and financial statements. The nature of management accounting is very flexible. Reports are not needed every week, month or need. When business require detailed report or statement then management accounting has enough time to prepare it with relevant information.

LSEC Ltd. to be an effective and profitable business needs to know the financial situation provided by management accounting. The aim of that department is to deliver relevant information which will place on a safe side finances of the company and will help to achieve organisational objectives. With all the new methods and systems management accountant is able to serve relevant information which later on will help into decision making. Businesses to be successful needs to have a plan. Lot of the companies in today’s world is using management accounting to find out where are their weak spots, because they want to improve all the processes.

Bibliography

Money Matters | All Management Articles. (2018). Concepts / Conventions of Management Accounting. [online] Available at: https://accountlearning.com/concepts-conventions-management-accounting/ [Accessed 4 Dec. 2018].

CGMA. (2018). Chartered Global Management Accountant. [online] Available at: https://www.cgma.org/ [Accessed 4 Dec. 2018].

principlesofaccounting.com. (2018). Planning, Directing, And Controlling – principlesofaccounting.com. [online] Available at: https://www.principlesofaccounting.com/chapter-17/planning/ [Accessed 4 Dec. 2018].

principlesofaccounting.com. (2018). Planning, Directing, And Controlling – principlesofaccounting.com. [online] Available at: https://www.principlesofaccounting.com/chapter-17/planning/ [Accessed 4 Dec. 2018].

Cite This Work

To export a reference to this article please select a referencing stye below:

Related Services

View all

DMCA / Removal Request

If you are the original writer of this assignment and no longer wish to have your work published on UKEssays.com then please click the following link to email our support team:

Request essay removal